Services & Products

Financial products traded by banks, securities firms, and other financial institutions—such as equities, bonds, and foreign exchange—can generally be categorized into two types: exchange-traded transactions, executed through organized exchanges, and Over-The-Counter (OTC) transactions, executed off-exchange, typically via specialized intermediaries.

OTC transactions, also referred to as off-exchange or bilateral trading, differ from exchange-traded transactions in that the terms are not necessarily standardized. Because OTC trades can be tailored to specific requirements, they offer greater flexibility in setting key conditions such as tenor, notional amount, and pricing.

An Inter-Dealer Broker (IDB) is a financial intermediary that facilitates OTC transactions between dealers at financial institutions, without using an exchange. IDBs connect market participants by matching counterparties and helping them execute trades efficiently.

In practice, an IDB receives offers and bids from client institutions—indicating trading conditions such as tenor, amount, and rate—then searches for a suitable counterparty and supports the parties in reaching an agreement and completing the trade.

Many of the financial products traded by banks and securities firms—such as cash equities, equity index futures, JGB futures, and USD/JPY spot FX—are highly standardized. For these products, electronic trading platforms are often the most efficient way to execute transactions, offering speed, transparency, and scalability.

By contrast, OTC derivatives, including Interest Rate Swaps (IRS), are generally non-standardized and typically traded among professional counterparties. Because the terms of each transaction can vary and market liquidity may be relationship-driven, these markets often benefit from direct communication and trust between participants. In such environments, Inter-Dealer Brokers (IDBs)—leveraging established dealer networks and human expertise—can facilitate transactions more efficiently and effectively than purely electronic execution.

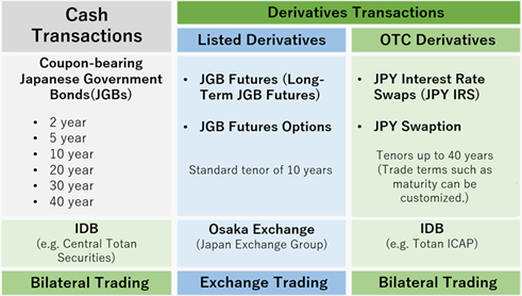

Financial products traded by financial institutions can be broadly classified into cash (spot) instruments—equities and bonds and derivatives, such as equity index and bond futures, which track the performance of their underlying cash markets.

To illustrate this, let us take the Japanese Government Bond (JGB) market as an example.

There are currently six types of interest-bearing Japanese Government Bonds (JGBs) outstanding: 2-year, 5-year, 10-year, 20-year, 30-year and 40-year bonds. Trading in these JGBs is classified as cash trading.

JGB futures are one type of derivative product. They were first introduced in October 1985 and are now listed on the Osaka Exchange, part of Japan Exchange Group (JPX). This futures contract is based on a 10-year “benchmark” JGB as the underlying asset. Derivatives listed and traded on an exchange in this manner are referred to as listed derivatives.

Options on JGB futures (“JGB futures options”) are also a type of derivative and are likewise listed on the Osaka Exchange.

By contrast, the financial products offered by our firm are derivatives traded bilaterally on an over-the-counter basis and are referred to as OTC derivatives.

Unlike exchange-traded transactions, which deal in standardized listed products, OTC transactions allow the terms of each trade to be adjusted freely by the parties involved. In the Tokyo interest rate derivatives market, the main product is the JPY IRS, which can be traded across a wide range of maturities—from as short as one day to as long as 40 years—offering a high degree of convenience and flexibility.

Yen interest rate swaptions, which are options on yen interest rate swaps, are another type of OTC derivative offered by our firm.

Our company is an IDB specializing in the intermediation of OTC derivatives transactions.

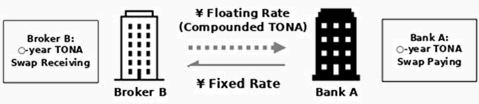

IRS is one type of derivative transaction. In a typical interest rate swap, two parties exchange different types of interest payments—commonly fixed interest for floating interest—within the same currency.

In the market, the fixed-rate leg is quoted and traded as the “price” of the swap. There is no exchange of principal; instead, only the net difference between the fixed and floating interest amounts is usually settled. The principal amount used for calculating interest on the swap is called the notional principal.

In the Tokyo interest rate derivatives market, the main product is the TONA swap, in which a fixed yen interest rate is exchanged for compounded TONA. A TONA swap is one type of yen IRS; the name of the swap varies depending on the type of floating rate referenced.

For US dollars, the main product is the SOFR swap, in which a fixed USD interest rate is exchanged for compounded SOFR. As these are OTC derivatives, the terms can be freely customized—ranging from swaps with a single settlement over a three- or six-month period to swaps with maturities of up to 40 years.

An interest rate swap in which different types or different maturities of floating rates in the same currency are exchanged is called a basis swap.

(Note) This differs from the USD/JPY cross-currency basis swap described later.

Below is an example of how a yen IRS can be used.

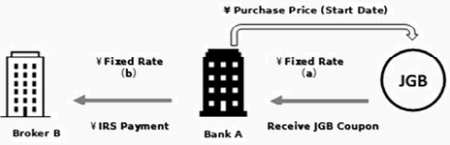

When Bank A purchases JGBs, it pays the purchase price and, in return, receives interest income from the JGBs. If Bank A expects that JGBs are likely to be sold off and that yields will rise, it can hedge the interest rate (price) risk on its JGB holdings by paying fixed on a yen IRS, without actually selling the JGBs.

Conceptually, the interest received from the JGBs (a) is offset by the fixed-rate payments on the yen IRS (b). Paying fixed on the yen IRS has the same economic effect as selling the JGBs.

If, at a later stage, Bank A then switches to receiving fixed on a yen IRS, this has the same economic effect as having sold the JGBs and then bought them back after the price decline.

In this case, because there is no exchange of principal in the yen IRS transaction, the amount of cash that actually needs to move is much smaller than in a transaction where the JGBs are sold and then repurchased.

Most of the interest rate options (IRO) offered by our firm are linked to JPY interest rates. The main types of interest rate options are swaptions, caps, and floors.

A swaption is an option transaction where the underlying is an interest rate swap—as the name suggests, it is a combination of a “swap” and an “option.”

For yen interest rate swaptions, the underlying is typically a TONA swap. A swaption is a transaction in which the right to enter into a TONA swap at a predetermined rate (the strike rate) on a specified future date is bought and sold, and a premium is paid as the fee for this right. If the buyer does not exercise the option, the seller of the swaption keeps the premium as profit.

The structure of a cap is similar to an insurance policy taken out to hedge against the risk of future interest rate increases, and the premium functions like an insurance premium. If interest rates do not rise above the specified level, the seller of the cap retains the premium as profit.

Conversely, a floor is a transaction in which a premium is paid for protection against the risk of future interest rate declines.

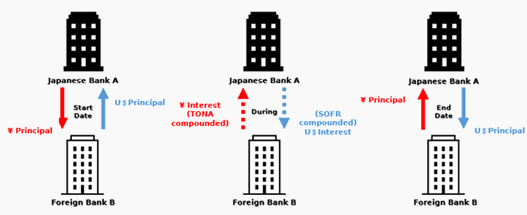

An interest rate swap in which principal and interest payments in different currencies are exchanged is called a Cross-Currency basis swap (XCCY basis swap). A USD/JPY cross-currency basis swap is one type of currency swap. In this transaction, the principals in the two currencies are exchanged at the start date and at maturity, and during the life of the swap, U.S. dollar floating interest and yen floating interest are typically exchanged every three months.

The U.S. dollar floating leg is based on compounded SOFR, and the yen floating leg is based on compounded TONA.

Although a USD/JPY XCCY basis swap involves an exchange of principal, it is a derivative that can be traded on a long-term basis.

Let us look at an example of how a USD/JPY XCCY basis swap is used.

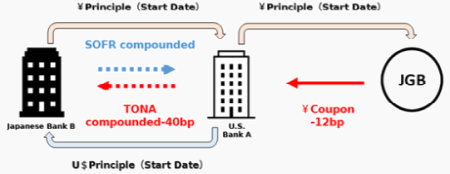

Suppose the two-year USD/JPY XCCY basis is quoted at minus 40 basis points (-0.40%). This means that, against compounded SOFR flat on the dollar leg, the yen leg pays compounded TONA minus 40 basis points, exchanged every three months.

The “minus 40bp” is the quoted price of the USD/JPY XCCY basis swap.

Now assume there is a U.S. bank A that can fund itself in U.S. dollars at compounded SOFR flat, and a Japanese bank B that wishes to obtain U.S. dollar funding.

If they enter into a two-year USD/JPY XCCY basis swap at -40bp, then U.S. bank A will lend dollars to Japanese bank B at compounded SOFR flat for two years, with interest settled every three months. In return, U.S. bank A will be able to fund itself in yen from bank B every three months at compounded TONA minus 40 basis points.

This reflects the strong demand for dollars: for Japanese bank B, obtaining dollar funding requires paying a "dollar premium" that is not included in the risk-free rate (RFR).

In other words, in exchange for being able to fund in dollars at compounded SOFR flat, Japanese bank B must effectively lend yen at a rate 40 basis points below compounded TONA as the dollar premium.

As a result, U.S. bank A can earn a sufficient spread even by purchasing, for example, a two-year Japanese Government Bond (JGB) yielding as low as -0.12% (-12bp), a level at which Japanese banks might hesitate to invest.

In cash transactions, the underlying and cash are exchanged at settlement. For securities such as equities and bonds, the settlement amount is calculated based on the prevailing market price at the time of the trade, and that amount is delivered and received. Investors can only purchase cash products within the limits of their own funds, and as a general rule, they cannot sell assets they do not own.

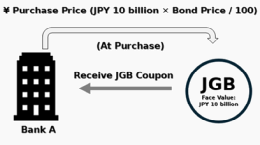

When purchasing a JGB in the cash market, the buyer pays the purchase price, which reflects the bond price in the market. For example, if Bank A buys JGBs with a face value of JPY 10 billion at a bond price of 101, it pays JPY 10.1 billion (there is an actual exchange of principal). This is what is meant by a cash transaction.

Derivatives are products derived from underlying financial instruments such as currencies, interest rates, bonds and equities, and are also referred to as financial derivatives. Types of derivatives include futures, options and swaps.

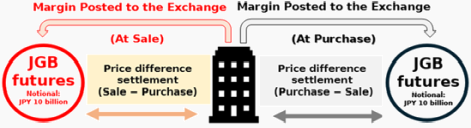

When purchasing JGB futures, the investor does not pay the JPY 10 billion notional amount to the exchange. Instead, the investor deposits margin with the exchange, which is much smaller than JPY 10 billion (there is no exchange of principal; only the difference between the purchase price and the sale price is cash-settled). Positions can be taken from either the long or the short side.

In this way, derivatives transactions usually involve no exchange of principal and are settled on a net basis.

As a result, derivatives can be traded with much less cash than cash transactions, allowing market participants to take exposure to a much larger notional amount.

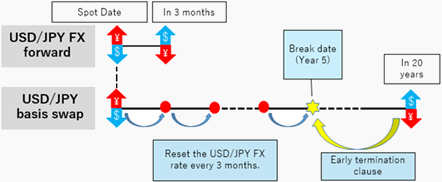

By contrast, a USD/JPY cross-currency basis swap involves an exchange of principal, yet it can be traded for long maturities that would generally be considered too long in a USD/JPY FX forward transaction. There are three main reasons for this:

| (a) As a rule, the USD/JPY FX rate is reset every three months. |

| (b) Collateral can be exchanged as needed. |

| (c) An early termination clause (a “break clause”) can be added where necessary. |

The most common tenor for USD/JPY FX forward transactions is three months. In a three-month USD/JPY FX forward, the principals in U.S. dollars and Japanese yen are exchanged on the spot date (two business days after the trade date), and the opposite exchange takes place three months later at maturity. If, after the trade is executed, the counterparty was to default and the USD/JPY spot rate had moved significantly, the non-defaulting party could suffer a substantial loss. For a one-year transaction, this risk is even greater.

In contrast, in a USD/JPY XCCY basis swap:

| • By resetting the USD/JPY FX rate every three months (point (a)), the transaction can be viewed as a series of consecutive three-month USD/JPY FX forwards. |

| • By exchanging collateral as needed (point (b)), |

| • And by including an early termination clause (a “break clause”) that, for example, allows a 20-year transaction to be terminated after five years (point (c)), |

the relative risk is reduced, making it possible to enter into long-term transactions.

TONA (Tokyo Overnight Average Rate) is the final weighted average rate (“final fixing”) of overnight (O/N) unsecured call transactions. It is calculated and published by the Bank of Japan based on data provided by three money market broker companies (Tanshi companies).

Because TONA is calculated from transactions that settle from “today” to the next business day, it is an overnight rate. To use TONA as a term reference rate for 1-month, 3-month, 6-month, 12-month and other tenors, it is necessary to compound TONA over the relevant period (compounded TONA)

A TONA swap is a swap in which, over a specified period, fixed rate(set in advance) is exchanged for interest based on compounded TONA (set in arrears).

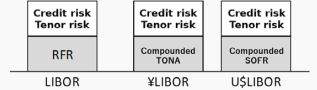

RFR (Risk-Free Rate) refers to an interest rate that reflects little or no bank credit risk in the context of bank funding.

For U.S. dollars, SOFR; for euros, €STR; and for pounds sterling, SONIA have been adopted as the RFRs for their respective currencies. These rates are calculated and published by each central bank based on actual funding transactions.

In general, the relationship between LIBOR, which has historically been used in the global financial markets, and the RFR can be illustrated as above. LIBOR is regarded as being composed of the RFR plus additional components such as credit and term risk.

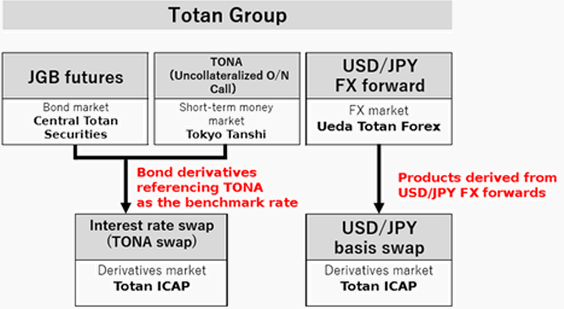

Within the Totan Group, Tokyo Tanshi Co., Ltd. operates in the short-term money market, Central Totan Securities Co., Ltd. in the bond market, and Ueda Totan Forex Co., Ltd. in the foreign exchange market, conducting and intermediating OTC cash transactions.

Cash transactions related to our business are as follows:

| (a) Uncollateralized overnight call transactions (commonly referred to as TONA): Tokyo Tanshi Co., Ltd. |

| (b) Cash JGB trading: Central Totan Securities Co., Ltd. |

| (c) USD/JPY FX forward transactions (mainly short-dated trades up to one year): Ueda Totan Forex Co., Ltd. |

Our company intermediates OTC derivatives transactions.

The interest rate swaps (TONA swaps) we broker are derivatives of bonds that reference TONA, and USD/JPY cross-currency basis swaps are derivatives of USD/JPY FX forward transactions. Both products can be traded from very short maturities of just a few days out to ultra-long maturities of up to 40 years.

The derivatives transactions we intermediate have the following characteristics:

| 1. The ability to take positions on larger notional principals |

| 2. The ability to trade across a wide range of maturities |

We have four trading desks: the Yen Swap Desk, the Basis Swap Desk, the Foreign Currency Swap Desk, and the Yen Interest Rate Options Desk.

Broadly speaking, the products we offer fall into three categories: IRS, XCCY basis swaps, and IRO.